The Hunt for Growth in Canada: 2.0

In this issue, we are continuing with the theme of “growth” in Canada with a deep dive into the material sector stocks first identified in the “Hunt for Growth in Canada” blog last month. Here is the list of the survivors from last month’s screen:

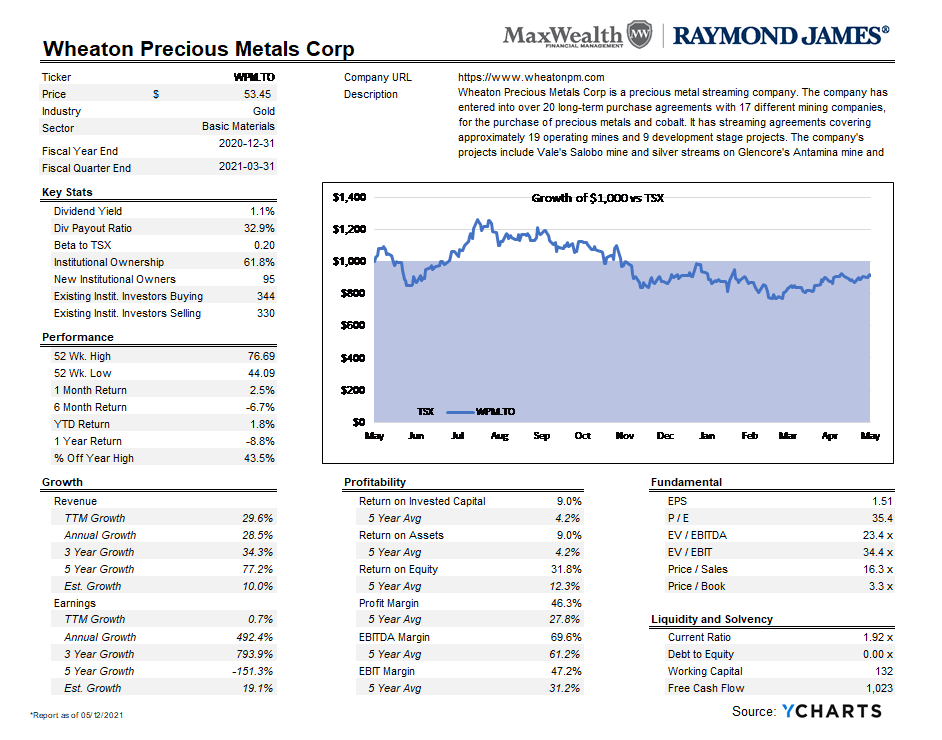

For those of you keeping score, Alamos Gold (AGI.TO) and Kirkland Lake Gold Ltd (KL.TO) were rejected due to negative earnings, revenue, and/or cash flow growth since the end of last month. The name we wish to highlight is Wheaton Precious Metals Corp (WPM.TO), because we currently hold this position in one of our models. Pictured below is a company snapshot of WPM.TO with some useful statistics.

While the debate continues on how to evaluate any security, we thought we would focus on the obvious strengths of Wheaton.

- Current quarter profitability measures are substantially greater than 5-year averages and trending favourably.

- Earnings growth is improving over the short-term. Clearly, this is a reflection of the improving economic environment for basic material stocks in general and precious metals in particular. This speaks directly to the reflation trade.

- WPM.TO has very little debt and last year’s free cash flow topped 1 billion CAD.

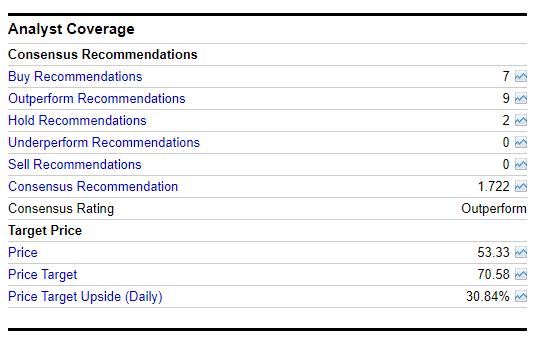

The next pieces of the puzzle are the analyst’s take on future earnings, revenue, and share price targets. As you can see, the consensus is quite favourable and the implied upside for share appreciation is roughly 30% from current levels:

Keep in mind these figures are just recommendations. Analysts often change their opinions over time and their accuracy can miss the mark. Regardless, this is just further evidence that WPM.TO has some of the qualities necessary for a suitable investment.

To round out our analysis, we like to review the technical picture of any potential candidate with a thorough investigation of its price chart. We believe that chart review is essential for better decision- making on when to enter or exit the physical trade. In summary, the price trend has improved since March as the longer downtrend of last July was broken to the upside. The 14-day RSI (relative strength index)—a measure of internal price momentum—is also consistent with further price upside. Typically, a reading of 70—as indicated last July—signifies price exhaustion. A reading in the 50s is considered a supportive one for price expansion. Finally, Wheaton shares are now above their 50-day moving average and are looking to challenge their 200-day. A move above this average would be considered bullish for the stock.

Given the above analysis, we believe that this security offers an attractive risk-to-reward equation. Obviously, gold stocks are not suitable for everyone’s portfolio or individual risk tolerances, but what our analysis illustrated was our multi-perspective process. First, we started with a quantitative screen that narrowed down the investible universe to a manageable number based on our specific criteria. Next, we looked under the hood of the business to see if the parts were all there and in good working order. Another term for this is fundamental analysis. Finally, we looked at the actual price movement over time to see if any profitable trends were emerging. We argue that this is the case. As you can imagine, thoughtful investing requires more than a dartboard and a series of sharp instruments for the decision-making process. We hope that our message finds you well and leads you down the road of profitable investing.

The enclosed article expresses the opinions of writer, Patrick A. Choquette, and not necessarily those of Raymond James Ltd. (“RJL”). Statistics, factual data and other information are from sources believed to be reliable but accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James Ltd. is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities.

Information provided in the attached report is general in nature and should NOT be construed as providing legal, accounting and/or tax advice. Should you have any specific questions and/or issues in these areas, please consult your legal, tax and/or accounting advisor.

Information in this article is from sources believed to be reliable, however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views are those of the author, Patrick Choquette, and not necessarily those of Raymond James Ltd. Investors considering any investment should consult with their Investment Advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision. Raymond James Ltd. is a Member - Canadian Investor Protection Fund.

![]()